Is a home inspection required for a conventional loan? This is a question that nearly 90% of prospective homebuyers end up asking. With a conventional loan being a type of mortgage that is not insured or guaranteed by the federal government, many people find it attractive mainly due to its flexibility and potential cost savings. The loans are offered by private lenders, such as banks and credit unions, and typically conform to the guidelines set by government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac.

When it comes to their classification, they are classified into conforming and non-conforming loans. Conforming loans adhere to the limits set by the Federal Housing Finance Agency (FHFA), while non-conforming loans, such as jumbo loans, exceed these limits. For the two categories, it is worth being aware that each has its own set of requirements and criteria that any borrower has to meet.

Key Takeaway

Is a home inspection required for a conventional loan? While a home inspection is not a mandatory requirement for obtaining a conventional loan, it is a highly recommended step in the home-buying process. A thorough inspection provides valuable insights into the property’s condition, helping buyers make informed decisions and negotiate better terms. Although the cost of an inspection may seem like an added expense, it is a worthwhile investment that can save buyers from significant financial burdens and ensure their new home is safe and habitable.

Home Inspection Explained

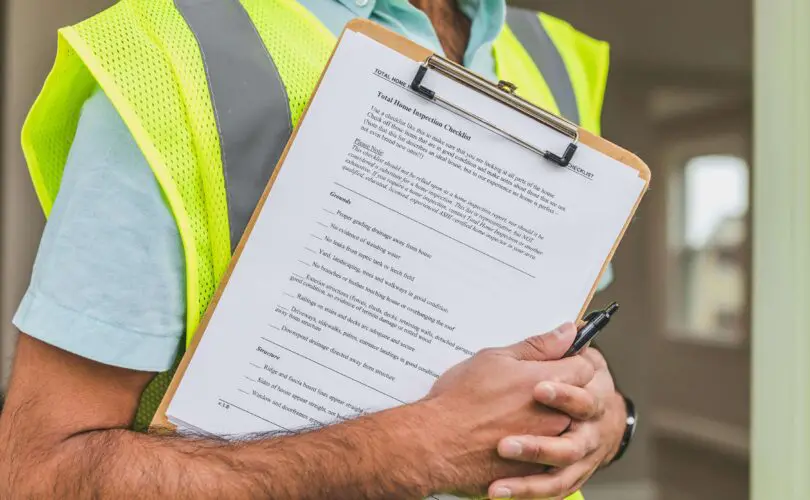

By definition, home inspection is a thorough examination of a property’s condition, conducted by a professional home inspector. The aim of such an undertaking is to identify any existing or potential problems with a property. This is an issue that has the potential to affect the value, safety, and livability of the property.

During the examination, the inspector evaluates different home aspects, including structural integrity, electrical systems, plumbing, heating and cooling systems, roof, foundation, and many others.

Doing the inspection assists in revealing any hidden issues that would not have been apparent during a casual walkthrough. Also, it serves as a source of peace of mind for the buyers since the risk of unexpected repairs after the purchase is reduced and an opportunity for negotiation leverage is made clear. The opportunity presents itself in that the buyer is able to use information concerning the issues related to the property to lower the purchase price or negotiate for repairs.

Above all, home inspections help in ensuring that a property meets the set safety standards, and protect the health as well as the well-being of the occupants. It would be risky to let people live in a property that is not safe and in which they could end up endangering their lives.

Conventional Loan Requirements: Are Home Inspections Mandatory?

Unlike some government-backed loans, such as FHA loans, conventional loans do not have a universal requirement for home inspections. However, it does not mean that home inspections are unnecessary or irrelevant in the context of conventional loans.

While conventional loan lenders do not typically require a home inspection, they often strongly recommend it. Their decision to recommend it is based on the understanding that both the buyer and lender are protected from any potential risks through the inspection.

Even with this being the case, there are things to take into consideration:

Lender Discretion

There are lenders who might have certain policies regarding home inspections. It is essential for borrowers to check with their lenders to understand any unique requirements or recommendations.

Property Appraisal vs. Home Inspection

It is important to differentiate between a property appraisal and a home inspection. A property appraisal is an assessment of the property’s market value conducted by a licensed appraiser, often required by lenders to ensure the loan amount does not exceed the property’s value. While an appraisal provides an estimate of value, it does not assess the detailed condition of the property like a home inspection does.

Risk Mitigation

Lenders aim to mitigate risks associated with lending on properties that might have significant defects by recommending home inspections. This practice helps maintain the quality of their loan portfolio and reduces the likelihood of borrower defaults due to unforeseen property issues.

Role of Home Inspections in Home Buying

Doing a home inspection prior to buying a property or during the buying process has a certain level of importance both from the buyer’s perspective and the seller’s perspective.

Buyer’s Perspective:

- Informed Decision-Making: A home inspection provides buyers with a comprehensive understanding of the property’s condition, enabling them to make informed decisions about their purchase.

- Financial Protection: Identifying potential issues before finalizing the purchase saves buyers from costly repairs and maintenance in the future.

- Negotiation Tool: Inspection reports are used to negotiate repairs or price adjustments with the seller, ensuring that buyers get a fair deal.

Seller’s Perspective:

- Transparency: Sellers who conduct pre-listing inspections demonstrate transparency and build trust with potential buyers.

- Faster Sales: Addressing issues before listing the property leads to quicker sales and smoother transactions.

- Reduced Renegotiations: Proactively addressing potential problems enables sellers to reduce the likelihood of renegotiations or delays during the closing process.

Cost of Home Inspection

Some of the factors that affect the cost of home inspection include the size of the property, its location, and the experience of the inspector. On average, the cost ranges from $300 to $500, for medium seized properties, meaning that the price is higher for larger and more complex properties.

For instance:

- Property Size: Larger homes require more time and effort to inspect, leading to higher costs.

- Location: The cost of living and demand for inspection services in a particular area can impact pricing.

- Inspector’s Experience: Experienced inspectors with specialized knowledge may charge higher fees.

Alternatives to Home Inspections

Despite being highly recommended, there are alternatives or additional measures that you as a home buyer might consider while assessing the condition of a property. The alternatives are:

1. Specialized Inspections

Specialized inspections focus on particular aspects of a property that may not be covered in a standard home inspection. Depending on the property’s age, location, and specific concerns, buyers may choose one or more of the following specialized inspections:

- Pest Inspections:

- Purpose: To identify the presence of pests, such as termites, rodents, or insects, that could cause structural damage or health hazards.

- Process: A licensed pest inspector examines the property for signs of infestations and conditions conducive to pests.

- Benefits: Early detection of pests can prevent extensive damage and costly repairs. It also ensures a safe living environment for the occupants.

- Structural Inspections:

- Purpose: To evaluate the structural integrity of the property’s foundation, framing, and other critical structural components.

- Process: A structural engineer or specialized inspector assesses the condition of load-bearing elements, looks for signs of settling or movement, and evaluates the overall stability of the structure.

- Benefits: Ensuring the structural soundness of a property can prevent future issues and expensive repairs. It also provides peace of mind regarding the safety and longevity of the home.

- Electrical and Plumbing Inspections:

- Purpose: To assess the condition and safety of the property’s electrical and plumbing systems.

- Process: Licensed electricians and plumbers inspect wiring, outlets, panels, pipes, fixtures, and other components to identify potential hazards or deficiencies.

- Benefits: Detecting issues early can prevent electrical fires, plumbing leaks, and water damage. It also ensures that the systems meet current safety standards and building codes.

Related Post: Can You Get an FHA Loan with an Eviction

2. Seller Disclosures

Seller disclosures are legally required statements provided by the seller that outline known issues or defects with the property. While not a replacement for a thorough inspection, they offer valuable insights into the property’s history and condition:

- Purpose and Content:

- Purpose: To inform buyers of any known problems or defects with the property, allowing them to make an informed decision.

- Content: Seller disclosures typically include information about past repairs, known issues with major systems (e.g., roof, HVAC, plumbing), any history of water damage or pest infestations, and compliance with local building codes.

- Limitations:

- Honesty and Knowledge: Disclosures are based on the seller’s knowledge and honesty. Some issues may not be disclosed if the seller is unaware of them or chooses not to disclose them.

- Scope: Seller disclosures may not cover all potential issues, especially those that are not immediately visible or have not been experienced by the seller.

- Benefits:

- Baseline Information: Provides buyers with a starting point for their evaluation and helps identify areas that may need further investigation.

- Transparency: Encourages transparency and trust between the buyer and seller

- Due Diligence: Allows buyers to perform due diligence and request additional inspections or negotiate repairs based on the disclosed information.

3. Walkthroughs with Contractors

Involving a trusted contractor or builder in the property evaluation process can provide additional insights into the condition and potential repair costs. Contractors can offer expert opinions on the property’s structural integrity, mechanical systems, and overall condition.

- Purpose and Process:

- Purpose: To gain a professional assessment of the property’s condition and identify potential repair or renovation needs.

- Process: During a walkthrough, the contractor will visually inspect the property, paying close attention to critical areas such as the foundation, roof, electrical and plumbing systems, and overall structural integrity.

- Benefits:

- Expert Insight: Contractors have the expertise to identify issues that may not be obvious to the average buyer or even a home inspector.

- Cost Estimation: They can provide rough estimates for necessary repairs or renovations, helping buyers budget for potential costs and make informed decisions.

- Renovation Planning: For buyers considering significant renovations, contractors can offer advice on the feasibility and cost of planned projects, ensuring that the property meets their needs and expectations.

- Limitations:

- Scope of Inspection: While contractors can provide valuable insights, their assessment may not be as comprehensive as a dedicated home inspection.

- Potential Bias: If the contractor is also bidding for the renovation work, there may be a conflict of interest. It’s important to choose an impartial contractor for the evaluation.